{kind=link}

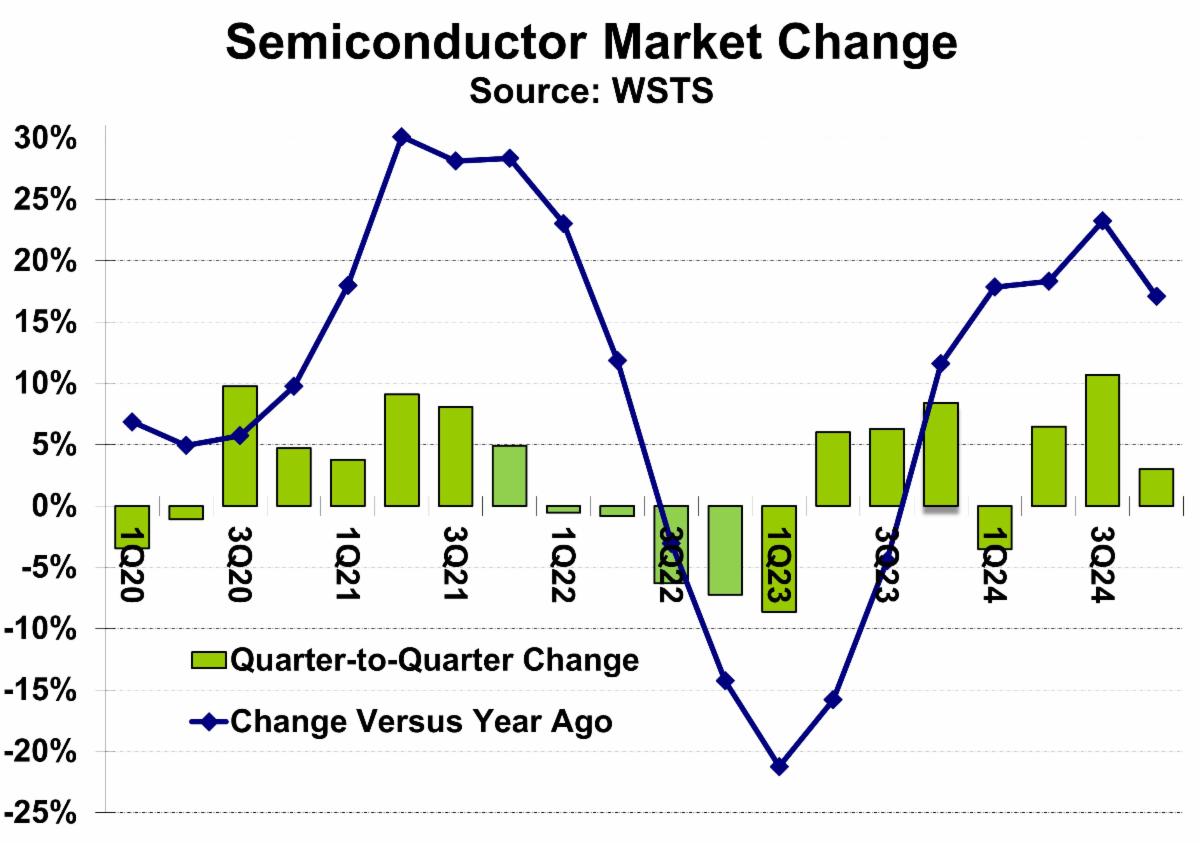

Probably the most correct analysts’ forecasts for final 12 months have been IDC which, in November 2023, projected progress of 20.2% for 2024 and the February 2024 forecast from Semiconductor Intelligence was 18.0%. The closing 2024 progress of 19.1% is midway in between. Different forecasts made on this interval ranged from 5% to 16%.

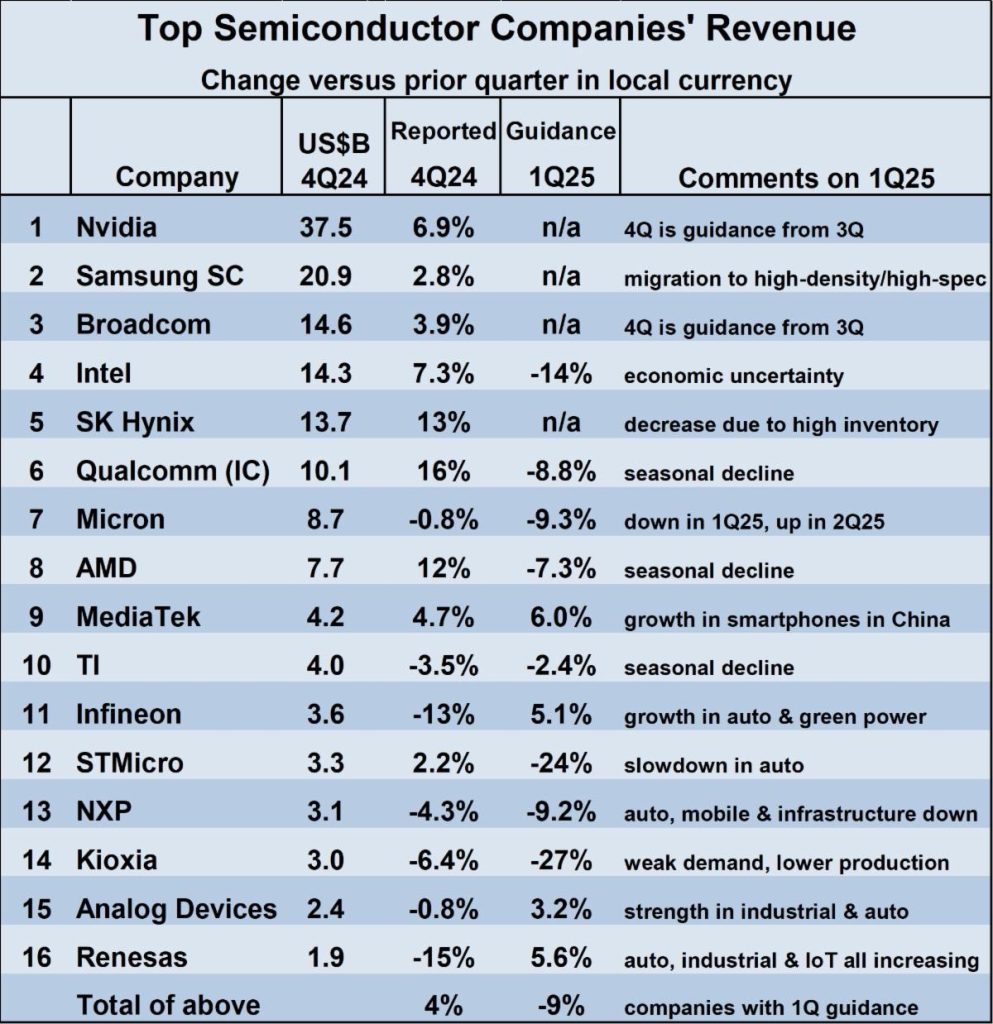

The 4Q 2024 income studies from sixteen main semiconductor corporations various extensively. 9 corporations reported elevated revenues in 4Q 2024 versus 3Q 2024. Three corporations – SK Hynix, Qualcomm and AMD – reported double-digit progress. Seven corporations reported declines, with Infineon Applied sciences and Renesas Electronics reporting double-digit declines.

The businesses offering steerage for 1Q 2025 income largely count on declines from 4Q 2024. MediaTek, Infineon, Analog Gadgets, and Renesas count on low-to-mid single-digit progress. The opposite eight corporations offering steerage count on declines, starting from minus 2.4% for Texas Devices to minus 27% for Kioxia.

Elements cited for the declines included seasonality, extra inventories, weak demand, decrease manufacturing and financial uncertainty. The weighted common income change for 1Q 2025 versus 4Q 2024 from the twelve corporations offering steerage was a 9% decline.

Over the past ten years, the semiconductor market has declined within the first quarter versus the fourth quarter 9 instances, starting from minus 14.7% to minus 0.5%, averaging minus 5%. The one first quarter improve throughout this era was 3.8% progress in 1Q 2021 throughout the restoration from the 2020 pandemic. Thus, the 1Q 2025 income steerage seems worse than typical seasonality.

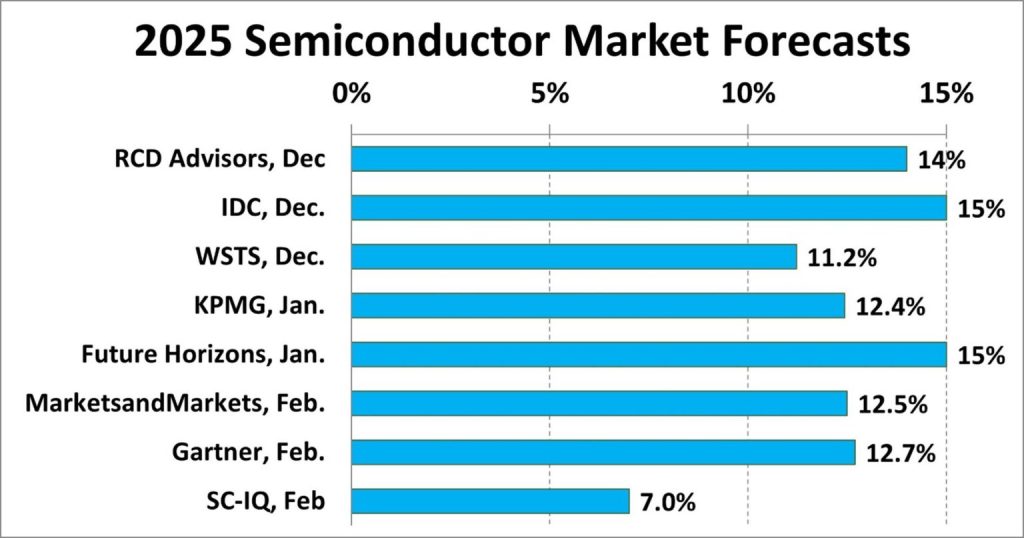

Given the anticipated sluggish begin to the 12 months, what’s the outlook for the semiconductor marketplace for the total 12 months 2025? Forecasts launched over the past three months vary from Semiconductor Intelligence’s 7.0% to fifteen% from IDC and Future Horizons. Our 7% forecast is an outlier, with different forecasts within the 11% to fifteen% vary.

The components driving SI’s conservative outlook for 2025 are:

AI servers drove a lot of the semiconductor market progress in 2024 as proven in our December 2024 publication. They need to stay robust in 2025, however at a considerably decrease progress price.

Key market drivers equivalent to smartphones, PCs, automotive and industrial stay weak.

The worldwide economic system is unsure in 2025 with the U.S. threatening elevated tariffs on imports and different nations promising retaliatory tariffs. Growing tariffs will improve prices for customers, probably leading to decreased demand and/or elevated inflation.